If you’re interested in stacking growth and steady income, low-cost high-yield ETFs are pretty appealing right now. These funds pull together a mix of dividend-paying stocks or bonds and deliver them in a package that’s not going to eat up all your returns with fees. I’ve spent hours sorting through platforms, reading fund sheets, and running screens to bring you an all-in-one look into how and where to track down these ETFs without spending tons of time or money.

Disclaimer: This article contains affiliate links. If you open an account through these links, I may earn a commission at no additional cost to you. Investing involves risk, including the possible loss of capital. eToro is not available in all countries. Eligibility depends on your region. Always consider your individual circumstances before investing.

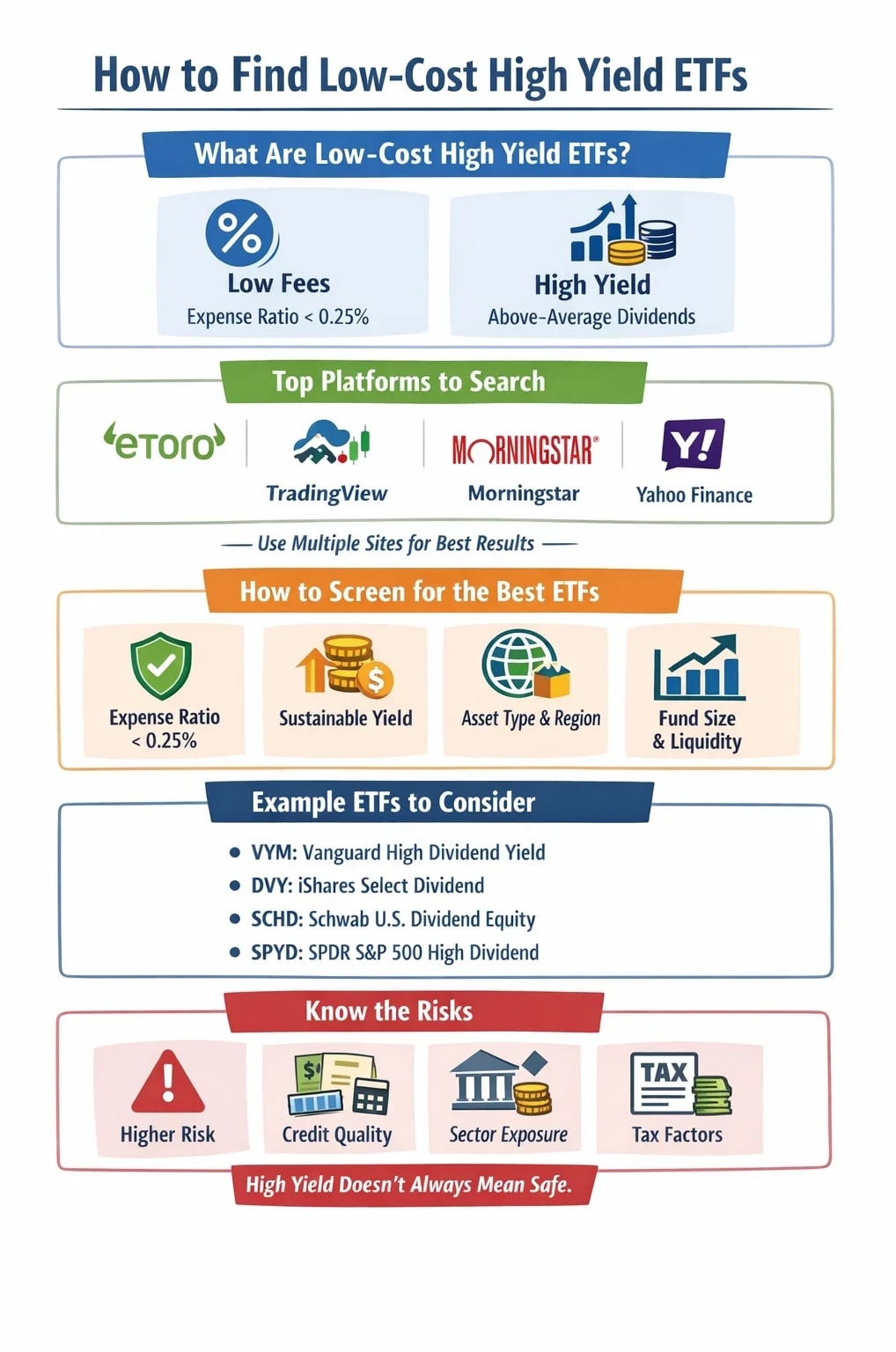

What Makes an ETF Low-Cost and High-Yielding?

A low-cost ETF keeps its fees pretty minimal; usually below 0.25% for expense ratios, sometimes even lower. That fee might sound tiny, but over time, it makes a noticeable difference in how much of your returns you actually get to keep. High yield just means the fund pays out a larger amount in dividends compared to the average ETF. These are usually backed by assets like real estate, utilities, or big dividend-paying companies, but sometimes you’ll find bond ETFs that offer higher-than-average interest payouts too.

It’s really important to remember, high yield doesn’t guarantee safety or performance. Sometimes higher yield shows a higher risk underneath. You still need to look under the hood and make sure the ETF fits your goals. More on those risks is available in my super detailed post: What Are the Risks of Low-Cost High-Yield ETFs?.

Popular Online Platforms for Finding Low-Cost High-Yield ETFs

Online brokers and financial research platforms make it much easier to scout for these kinds of ETFs. Here are a few spots I use regularly, including some affiliate partners that help keep my research free for readers:

- eToro: This platform’s ETF screener is pretty handy for filtering by fee and yield. I’ve found it way less clunky than some old-school broker sites. Check them out here.

- TradingView: Besides their famous chart tools, TradingView offers a clean ETF search and good dividend stats. Worth seeing for yourself here.

- Morningstar: They’ve got a deep data set for ETFs, including fees, yields, and performance history, but require an account for full access.

- Yahoo Finance: Handy for casual searching. Ticker lookup is totally free, and yield/fee breakdowns are updated regularly.

I like to use two or three of these to cross-check info before settling on any picks. Some brokers and research tools will even let you set custom alerts when new high-yield, low-cost funds hit the market, which is pretty useful for keeping tabs on new opportunities. As the ETF universe keeps growing, these platforms also regularly introduce new screening features or data visualizations to help you find better picks much faster. By taking advantage of different sites, you can get extra verification that the data is accurate and up to date.

How to Search and Screen for the Best Options

The key to finding top low-cost high-yield ETFs is smart screening. Most sites above include filters for expense ratio and dividend yield. I usually set the expense ratio slider all the way down to 0.25%, and sort dividend yield from high to low. Make sure to read the ETF profile page. Some funds report “trailing 12-month yield” or “SEC yield,” which are both good ways to judge income, but read what each metric means. This can help you avoid confusion about how much money you’ll truly receive in dividends.

Other filters I recommend using:

- Asset type: Are you after stocks, REITs, or bonds? Narrow it down, as different asset classes have different risk and yield levels.

- Geography: U.S. funds tend to have more transparency and lower costs; international funds can sometimes edge out higher yields if you’re looking globally.

- Liquidity: Stick to funds with good average daily trading volume so you won’t get stuck with huge spreads when buying or selling.

- Market cap and size: Larger funds with more assets under management usually have better liquidity and lower trading costs. Double-check the fund size if you plan on investing a substantial amount.

For step-by-step guidance on comparing investment options, check out my post: How to Evaluate Low-Cost High-Yield ETFs Investment Options.

Real World Examples: ETFs I’ve Found Using These Platforms

After plenty of screen time testing, here are a few ETFs that usually pop up in screens for low fees and high yield:

- Vanguard High Dividend Yield ETF (VYM): Expense ratio around 0.06%, yield around 3% recently, and lots of big, stable companies inside.

- iShares Select Dividend ETF (DVY): Expense ratio about 0.38% (slightly higher), yield lately sitting near 4%, focusing on mature, dividend-paying companies.

- Schwab U.S. Dividend Equity ETF (SCHD): Expense ratio 0.06%, yield close to 3.5%, very popular for a reason.

- SPDR Portfolio S&P 500 High Dividend ETF (SPYD): Expense ratio 0.07%, yield often between 45%, with more focus on the highest-paying S&P stocks.

You can find these on all the platforms above just by using their ticker symbols in the search bar. If you want to compare their performance charts, most broker platforms make it easy to stack ETF returns, volatility, and dividend payouts side by side for a closer look.

Important Things to Watch Before Investing

Low costs and high yields don’t automatically make an ETF a slam dunk. There are a few things I always double-check first:

- Dividend sustainability: Is the ETF paying out from real earnings, or is it dipping into capital to look good? Too good to be true rarely lasts.

- Credit quality (for bond ETFs): High yields on bond funds can sometimes mean they load up on risky, low-rated bonds.

- Sector exposure: Some high-yield ETFs might be heavy in sectors like energy or real estate, which can mean more ups and downs if that sector struggles.

- Fees and taxes: Even low fees can add up. Non-U.S. funds may have extra tax considerations, so keep those details in mind.

If you’re trying to figure out when to time your ETF buys for maximum yield, my post here comes in handy: When to Buy Low-Cost High Yield ETFs for Best Results. Watching ex-dividend dates in particular can help you secure upcoming payouts with better timing.

Common Questions About Low-Cost High-Yield ETFs

How safe are low-cost high-yield ETFs?

Safety depends on the fund’s holdings, not just the fees or yield. Funds loaded with risky bonds or supervolatile stocks can pay more, but they might drop in value faster if markets wobble. Always look into the underlying holdings. For a breakdown of common pitfalls, visit my post: What Are the Risks of Low-Cost High-Yield ETFs?.

What counts as a “high yield” for an ETF?

For U.S.-listed stock ETFs, anything over 3% is seen as worthwhile. Bond funds can go higher, but anything above 56% deserves extra research to see whether the risk is worth it.

Can I use these for retirement income?

Many investors add these ETFs to their IRAs or retirement accounts to build up regular income. Just keep an eye on tax stuff and rebalance every so often to keep your risk and yield in the sweet spot. Building up a mix of ETFs from different sectors or asset classes can also make your income stream more resilient.

Are there any good international options?

Yes, a few global and emerging market options offer high yields, but fees are sometimes a bit higher, and volatility can be higher too. Compare several picks to see what fits, and make sure you check currency risk and tax treatment in your home country before adding international funds.

Tips for Boosting Your ETF Search Strategy

Once you’ve got a handle on screening, there are a few practical moves I’ve found that really help:

- Set up watchlists: Platforms like TradingView and eToro let you save ETFs to watch and alert you when yields or prices switch up.

- Check fund updates: Review quarterly reports to spot any changes in dividend policies or sector weighting. These updates can remind you if the ETF’s yield is slipping or if fees increase.

- Balance yield with risk: It’s tempting to snag the biggest dividend, but too much in one sector or super high-yield funds can add up to a bumpy ride over the long term. Mixing in different types of ETFs can smooth out these bumps.

- Review tax implications: With international ETFs or those in taxable accounts, dividends can get taxed at different rates, so make sure to check your country’s rules if you’re investing on a global scale. Don’t overlook dividend withholding taxes on foreign ETFs, as they can eat into your returns over time.

Another handy tip: Use portfolio simulators or ETF comparison tools online to see how different mixes of these ETFs could have performed together in past years. This can give you a sense of how adding a new fund might affect your total returns or volatility over time. Sites like Portfolio Visualizer even let you stress-test how your portfolio would have held up in past downturns.

Final Thoughts

Finding low-cost, high-yield ETFs is mostly about using the right research tools and being clear on what you’re after. I like to stick with platforms that make screening and tracking easy, then narrow the list by double-checking yield stability, underlying assets, and cost over time.

There are plenty of low-fee, income-boosting ETFs out there if you’re willing to do a bit of homework up front. If you keep an eye on cost, yield, and risk, you’re more likely to end up with an ETF that can help you reach your income or growth needs for the long term. Remember, it’s not just about grabbing the top numbers; choosing funds that keep costs low and risks manageable is key to building up consistent returns.

Anytime you spot a new fund that catches your eye, walk through those filters and review fund documents before jumping in. If you use the affiliate links above, it helps me keep digging up new research and sharing what works. Here’s to finding the right mix for your portfolio and getting the income you want—without giving up too much in fees or safety.