If you’re eyeing steady income from your investments, low-cost, high-yield ETFs can look really appealing. These ETFs are known for their above-average dividend yields and low management fees, which make them more affordable compared to many traditional funds. Before making a move, it’s worth understanding what kind of average return you could expect, what drives those returns, and what factors to watch out for when choosing a fund. These considerations will help you get the most out of your investment plans and avoid common mistakes.

Disclaimer: This article contains affiliate links. If you open an account through these links, I may earn a commission at no additional cost to you. Investing involves risk, including the possible loss of capital. eToro is not available in all countries. Eligibility depends on your region. Always consider your individual circumstances before investing.

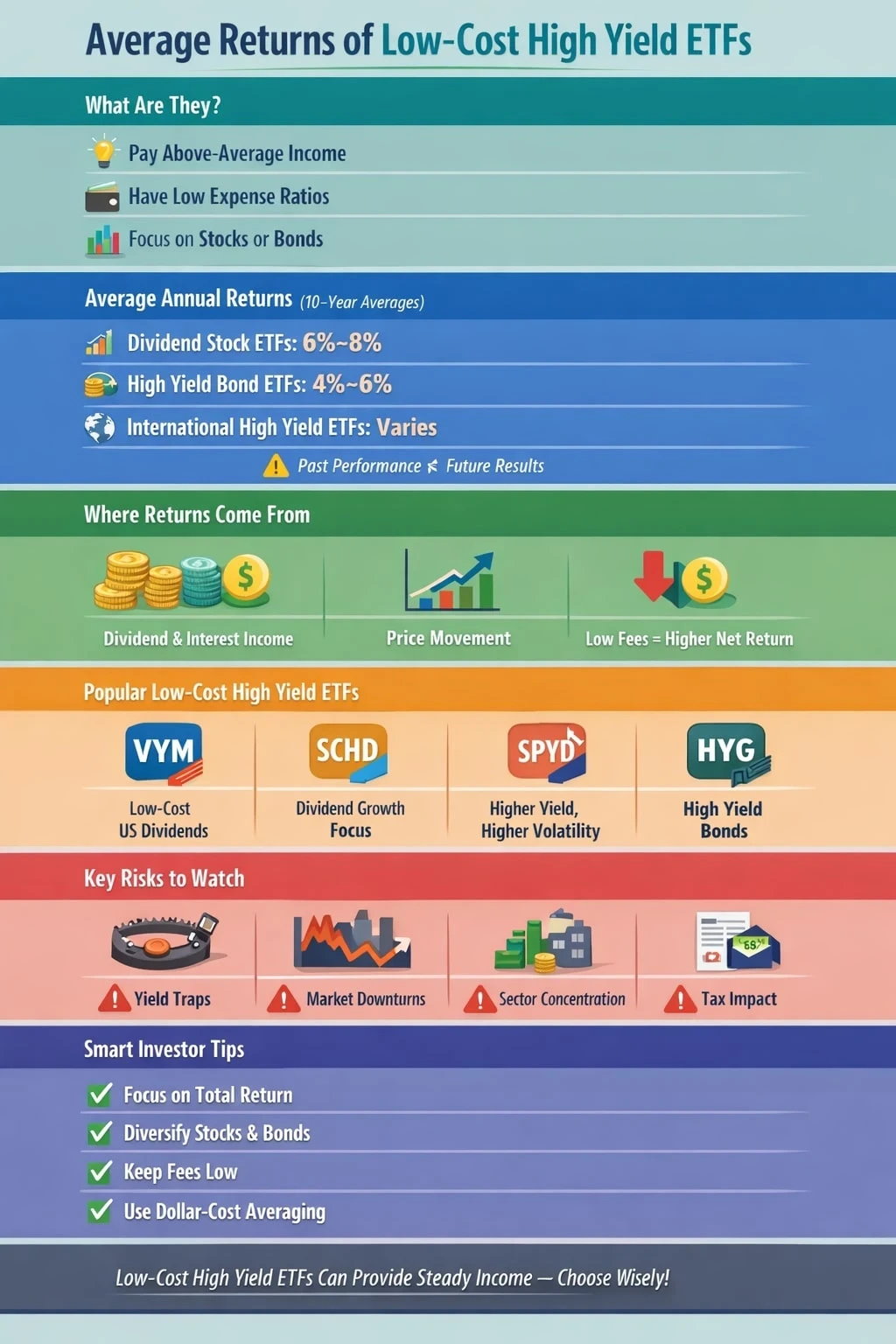

How Average Returns on Low-Cost High-Yield ETFs Work

Low-cost high-yield ETFs usually focus on stocks, bonds, or assets that pay regular dividends or interest. The “low-cost” part comes from having expense ratios (the annual fee you pay to own the fund) much lower than traditional mutual funds or actively managed ETFs. Over time, those lower fees can add up to a real difference in your overall returns.

The “high yield” side means you get paid more in dividends or interest compared to broader market ETFs. That income can be especially attractive for folks looking for cash flow, like retirees or anyone wanting to supplement their regular earnings. Also, the simple structure of these funds tends to make them user-friendly and accessible to investors of all experience levels.

Historical Average Returns: What to Expect

Over the last decade, most broad-market high-yield ETFs with low fees have produced total annualized returns that sit between 4% and 8%. This range factors in dividend payouts plus price appreciation (or losses, during tough years). For example, some popular low-cost ETFs focusing on U.S. high-dividend stocks, like the Vanguard High Dividend Yield ETF (VYM), usually show returns around 6.5% to 7.5% a year when averaged out over ten years.

Bonds-focused high-yield ETFs (like those holding corporate or emerging market bonds) sometimes push yields towards the higher side, but with extra risk. Their average annual performance has generally trailed stocks over the long run, often staying in the 4% to 6% range, factoring in all the ups and downs. Furthermore, international high-yield ETFs—those that give access to global companies or sovereign debt—may offer different return profiles and diversification benefits, though they sometimes come with currency risk or unique economic challenges.

Just remember, past averages don’t lock in future results. Markets change over time, interest rates jump around, and some years might serve up losses even for yield-focused ETFs. Keep this in mind and always double-check current fundamentals before making a decision.

Main Drivers of Returns in High-Yield ETFs

Low-cost high-yield ETFs make money (and pass that money to you) through:

- Dividend payments or bond interest: This is the steady cash flow part. Strong, consistent income helps cushion portfolios during slower market years.

- Price changes: The value of the underlying stocks or bonds can go up or down. If the market does well, you might see bonus growth on top of the yield. If it stumbles, you could see smaller returns or even a loss for that year.

- Expense ratios: Lower annual fees let you keep more of the gross yield. Even a 0.5% difference in expenses adds up over several years.

The real trick is mixing steady yield with investments that won’t get crushed during market downturns. That’s where lots of research and a bit of patience come in handy. Understand that sometimes defensive sectors, such as consumer staples, healthcare, and utilities, provide the income stability these funds need, while cyclical sectors like energy or finance can set you up for bigger gains—and bigger risks—when market cycles switch up.

Popular Low-Cost High-Yield ETFs To Check Out

Every investor’s goals are different, but here are a few funds I find worth checking out when you want high yield without paying big fees:

- Vanguard High Dividend Yield ETF (VYM): Tracks U.S. companies with above-average dividends. Last decade returns are around 6.8% per year. Expense ratio: 0.06%.

- iShares Core High Dividend ETF (HDV): Focuses on U.S. blue chip dividend stocks. Recent annualized returns sit around 6.5%. Expense ratio: 0.08%.

- Schwab U.S. Dividend Equity ETF (SCHD): Solid for dividend growth and income, with a 10-year average return close to 11% (helped by big stock bull runs). Expense ratio: 0.06%.

- SPDR Portfolio S&P 500 High Dividend ETF (SPYD): Offers high yield by focusing on higher-paying stocks in the S&P 500. The annualized average is about 7% over the past decade. Expense ratio: 0.07%.

- iShares iBoxx $ High Yield Corporate Bond ETF (HYG): For those into bonds, this one pays a higher interest yield but has more risk. Long-term annual returns hover around 4.5%–5.5%. Expense ratio: 0.49%.

You can find more details and compare tickers on sites like TradingView and eToro. Up-to-date performance stats from these platforms can make sorting choices much quicker for investors.

Things To Really Think About Before You Buy

Pursuing high yields sounds nice, but there are some practical things to watch for. If you’re interested in exploring more cases for and against investing right now, check out this guide on when to get started with low-cost high-yield ETFs.

- Yield Traps: Superhigh yields might mean higher risk or a recent price drop. Sometimes those yields aren’t sustainable, so checking the source of the yields is pretty important. Don’t just trust the percentage—track down how the ETF gets its yield and check if the companies or bonds are in good shape.

- Market Swings: High-yield stocks or risky bonds sometimes fall harder in recessions. That income can dry up if dividends are slashed or defaults pile up. Stay aware of broader economic trends and how sensitive your chosen sectors might be to downturns.

- Sector Concentration: Some funds load heavily into a few industries (like utilities, energy, or financials). That can work fine during good times, but it adds risk if those sectors hit a rough patch. You can smooth the way by combining funds across sectors or looking for ETFs with more even exposure.

- Tax Efficiency: Dividends paid by ETFs might be taxed at different rates; it’s worth comparing if you’re working with taxable accounts. Some international ETFs may be subject to foreign withholding taxes, too, so check the tax treatment in your region.

Curious about risks? I talk about more in my full guide to ETF risks.

Yield Versus Total Return

Chasing only the top yield number isn’t always the best move. It’s really important to look at total return, which includes both the income you get and price movement over time. Sometimes a smaller dividend plus growth ends up ahead of just raw high yield, especially after factoring in taxes and inflation. Think about your goals—is it just cash flow, or do you want long-term growth along with steady income?

Expense Ratios: Why Low Cost Still Matters

Expense ratios are just the annual fees taken from the fund’s assets. Low-cost funds almost always leave more money in your pocket, year after year. Make sure to compare these numbers when you’re picking between similar ETFs. A few extra tenths of a percent in fees can shrink your returns pretty fast over a decade. Even if two ETFs look almost identical, if one is a little cheaper over time, you end up holding on to more of your gains—it’s that simple.

Building a Portfolio With High-Yield ETFs

Low-cost, high-yield ETFs can be great building blocks in any portfolio. Some people use them for core income, while others mix them in for extra diversification. I’ve found that spreading investments across a couple of different ETFs (like going with both stock and bond yields, or mixing in domestic and global funds) can help balance out risk. A mix like this not only keeps your cash flow steady but also helps protect your investments from single-sector shocks.

Timing also matters. For those thinking about when to buy, check out my article on timing your ETF investments for a few tips to boost your odds of starting on the right foot. Also, consider using dollar-cost averaging—putting in money at regular intervals—to reduce the impact of volatility in the price of your chosen ETFs.

Frequently Asked Questions

Here are answers to a few popular questions about low-cost high-yield ETFs:

What’s the average return of a low-cost high-yield stock ETF?

For most U.S.-focused low-cost high-yield stock ETFs, average long-term annual returns tend to fall between 6% and 8%, with a decent amount of that coming from dividends. These returns are not guaranteed, so always check current fund performance before you invest.

Are high-yield bond ETFs riskier than dividend stock ETFs?

Generally, yes. High-yield (a.k.a. junk) bond ETFs have higher default risk, and their price swings more with economic cycles. The payout can be higher, but you’re taking on more risk. Assess your own risk tolerance and make sure it matches the fund’s profile.

How often do high-yield ETFs pay out income?

Most pay quarterly, but some offer monthly distributions. Always check the fund’s payout schedule before you buy if you’re counting on regular cash flow. Monthly payers can be handy for budgeting, while quarterly funds may be more conventional in their approach.

Does a higher yield always mean better returns?

Not always. Sometimes, a high yield just means a stock or bond lost value and its payments represent a bigger share of the price. It can also point to greater risk, so don’t just buy for the number—dig into what’s driving the yield and be sure you’re comfortable with the reasons behind it.

Wrapping Up

Low-cost high-yield ETFs offer regular income with minimal management fees, which is a pretty attractive combo for lots of investors. Their average returns are shaped by market conditions, the types of assets in the fund, and, of course, how much risk you’re willing to shoulder. As always, diversification, timing, and ongoing research make a big impact.

If you’re interested in tracking down actual returns or want to compare funds side by side, platforms like eToro and TradingView are super useful places to start your search. Building an income-focused portfolio is definitely possible with these ETFs. Just make sure you’re clear on your goals and the risks you’re ready to handle. And if you ever feel unsure, don’t hesitate to ask a financial advisor or do some more research before making your choice.