If you spend any time looking into investing or building passive income, ETFs end up on your radar pretty fast. With so many options, figuring out exactly what a low-cost high-yield ETF is can make a big impact on how you approach growing your money. I’m going to break down what these ETFs are, how they work, and why so many folks are into them—even if you’re totally new to investing.

Disclaimer: This article contains affiliate links. If you open an account through these links, I may earn a commission at no additional cost to you. Investing involves risk, including the possible loss of capital. eToro is not available in all countries. Eligibility depends on your region. Always consider your individual circumstances before investing.

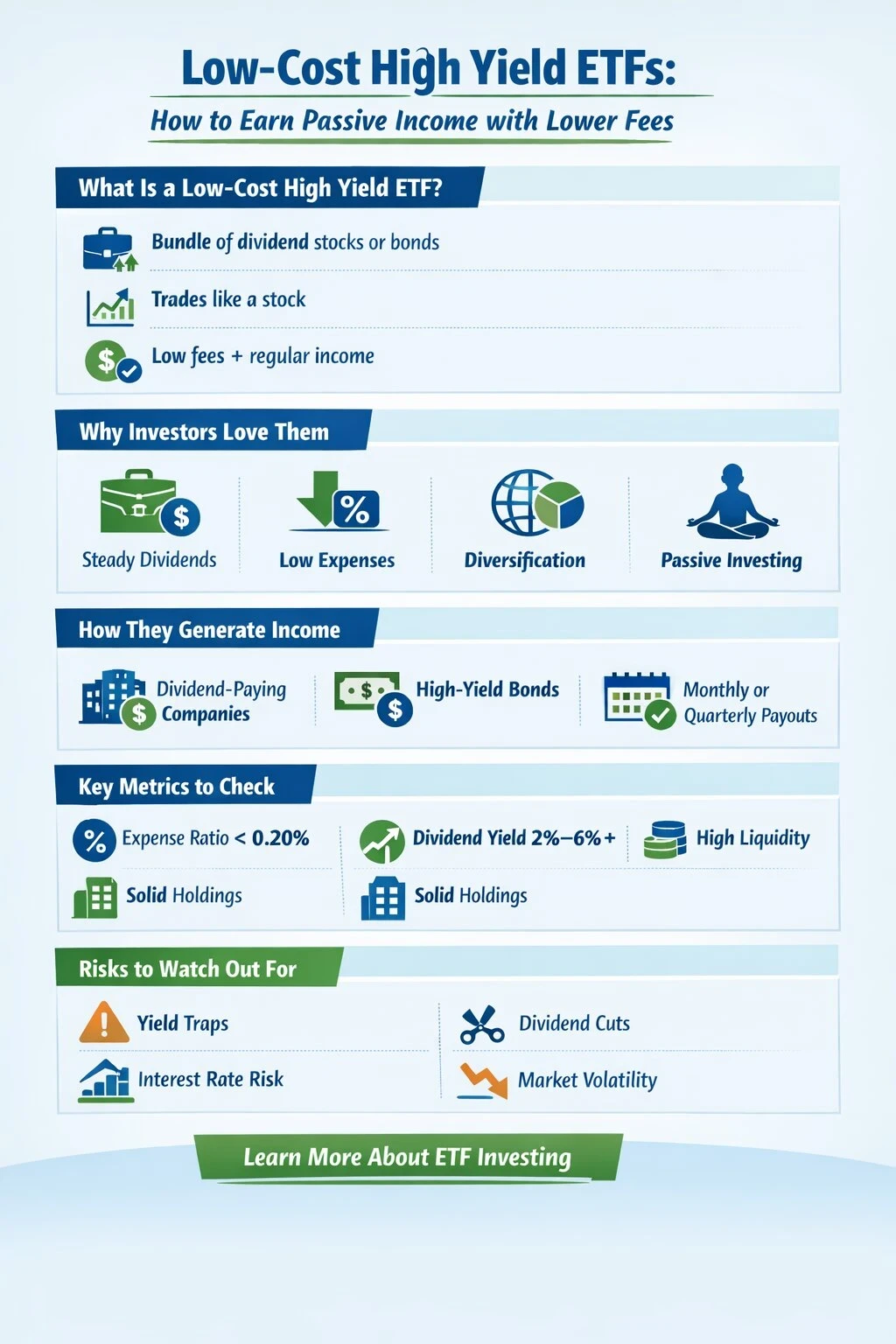

What Does “Low-Cost High-Yield ETF” Mean?

An ETF, or exchange-traded fund, is a bundle of investments (like stocks or bonds) that you can buy all at once, just like you’d grab a pack of drinks instead of buying cans one at a time. A low-cost ETF is simply one that doesn’t charge you much in fees to own it. High yield means the fund tries to pay out bigger dividends or interest income compared to regular ETFs.

The combo of low cost and high yield is something lots of investors look for. You get to keep more of your earnings thanks to the lower fees, and you get potentially bigger payouts. That’s pretty attractive if your goal is to make your money work for you without getting eaten up by expenses.

How Do Low-Cost High-Yield ETFs Work?

These ETFs usually focus on collections of companies or bonds known for paying good dividends. The “low-cost” bit usually refers to the fund’s expense ratio. That’s the percentage of your money the fund takes every year to cover management and other costs. You’ll notice low-cost ETFs often have expense ratios under 0.20%, sometimes even less.

High-yield ETFs pull together stocks from companies that hand out high dividends, or they focus on higher-yielding bonds. Instead of you buying a ton of these individually, the ETF does the work, and you just hang onto the fund. Then, you collect dividend payouts (sometimes monthly, sometimes quarterly), which you can either pocket or use to buy even more shares automatically.

Why Investors Like Low-Cost High-Yield ETFs

There are a couple of reasons why these ETFs are pretty popular, even with beginners:

- Steady Income: High-yield ETFs make a habit of spitting out regular dividends, which is great for income-focused investors or anyone trying to grow wealth steadily.

- Lower Fees: Since the expense ratios are low, you’re not constantly losing money to management costs.

- Diversification: Instead of relying on a single high dividend stock or bond, you get a whole basket, so you’re less exposed if one company or bond takes a hit.

- Passive Management: Most low-cost ETFs are passively managed; that means they’re just tracking an index or set formula, so you don’t need to stress about someone making risky trades with your money.

Main Features of a Good Low-Cost High-Yield ETF

If you’re trying to spot a high quality low cost high yield ETF, these details are good to keep an eye on:

- Expense Ratio: Lower is better here. Anything under 0.20% is pretty competitive.

- Dividend Yield: This number tells you what percentage of your investment you’re likely to get back each year as income. You’ll find options between 2%–6% annual yield, sometimes more.

- Holdings: Check out what’s inside the ETF. Are most of the holdings in reliable, dividend-paying companies? Is the bond quality reasonable?

- Liquidity: Can you buy and sell shares easily without pushing the price all over the place? Bigger ETFs with high trading volume are usually less hassle.

- Distribution Schedule: Some pay dividends monthly, some quarterly. Pick what fits your needs best.

Common Types of Low-Cost High-Yield ETFs

You’re probably going to see a few different “flavors” of high-yield ETFs. Here are the big categories:

- Dividend Focused Stock ETFs: These bundle up dividend-paying stocks, often focusing on stuff like utilities, banks, energy, or real estate companies that pay out regular income.

- Bond ETFs: Hunt for bonds that offer higher interest rates, like corporate bonds or junk bonds (which are riskier but tend to pay more).

- Covered Call ETFs: These are a bit advanced. They generate yield by selling options on the stocks they own. Yield can be good, but there are extra risks.

If you want some ideas for strategies beyond just buying the basics, here’s a deeper look at innovative approaches to high-yield ETFs that are worth checking out.

Challenges and Things to Watch Out For

While low-cost high-yield ETFs can be pretty handy, some details deserve a closer look:

- Yield Trap: Super high yields can sometimes be a red flag, like a company that’s in trouble and has to offer bigger payouts to attract buyers.

- Dividend Cuts: If companies in the ETF run into problems, they might drop their dividend payments, lowering your yield.

- Interest Rate Risk: For bond-focused ETFs, rising interest rates can eat into their value.

- Tax Treatment: High yield, especially from bonds, can mean higher yearly taxes depending on where you live.

- Market Risk: Like all investments, your money is at risk. Even a diversified ETF can lose value if the whole market takes a hit.

Careful research helps buyers make more informed decisions. If you’re exploring niche corners of the ETF world, this guide to niche ETF strategies offers maximizing returns.

How to Start Investing in Low-Cost High-Yield ETFs

Getting started isn’t tough, but having a step-by-step plan is super useful. Here’s how I recommend approaching it:

- Pick Your Platform: Sign up with a brokerage that offers a solid range of ETFs with low (or zero) commissions. I personally found eToro is pretty beginner-friendly, and TradingView is awesome for research and charting.

- Do Your Homework: Look at expense ratios, yield, liquidity, and what the fund actually invests in.

- Decide Your Allocation: Figure out how much of your portfolio you want in income-generating funds compared to growth or other investments.

- Buy in Small Chunks: You can always start small and add more as you feel comfortable.

- Reinvest or Take the Cash: Decide up front if you want your dividends paid into your account or automatically reinvested into more shares (called DRIP, dividend reinvestment plan).

It’s always good to review your holdings every once in a while to make sure you’re still happy with the costs, the yield, and the risk levels. Consider rebalancing your portfolio once or twice a year, especially if your goals change or the market gets rocky. Setting reminders can be handy to keep up with how your ETFs are performing.

Useful Real-Life Scenarios

Here are a couple of ways these ETFs fit into real portfolios:

- Building Passive Income: Retirees and FIRE (Financial Independence Retire Early) folks look at high-yield ETFs for steady, hands-off cash flow.

- Balancing Risk: Younger investors might pair high-yield ETFs with more growth-oriented funds to balance growth and income.

- Automatic Savings: Setting up auto investing and letting the ETF pay regular income straight into your account.

If you want to peek further into where ETFs are headed, checking out news on the future of ETFs in the digital economy gives some perspective on how new technology is changing the ETF world. Digital advisors now help people automate their investments, and smart ETFs are bringing AI into the mix, which could set investors up for even more hands-off income in the future.

Frequently Asked Questions

Here are some questions I hear all the time from new investors:

Q: Are low-cost, high-yield ETFs safe?

A: They do lower risk with diversification, but you’re still exposed to market swings and dividend cuts. Safer than single stocks, but not risk-free.

Q: What’s the difference between an ETF and a mutual fund?

A: ETFs trade all day like stocks, often cost less, and you can buy even just one share. Mutual funds trade just once after the market closes each day and can have higher fees.

Q: Can I lose money in a high-yield ETF?

A: Yes, especially if the market drops, interest rates spike, or companies inside the ETF cut their dividends. Diversification helps, but it’s not a guarantee against losses.

Q: Is now a good time to buy into high-yield ETFs?

A: Timing the market is super tricky. The best move is usually to start slow, keep learning, and stick with your plan for the long run.

Final Thoughts

Low cost high yield ETFs are a flexible option if you’re looking for both income and low fees. They’re a way to build passive cash flow, save on management costs, and spread out your risks. Remember to do your homework, pick the right mix for your goals, and review your investments from time to time. If you’re ready to start, test out platforms like eToro or do your research with TradingView to make the most of your ETF ride.