If you’re looking to invest without paying through the nose in fees, low-cost ETFs are pretty much the top pick for many individual investors. These exchange-traded funds aim to give you broad market exposure or access to specific sectors and strategies, but with management fees so low you barely notice them. I’m going to break down what I’ve learned by using them in my portfolio, so you can get a sense of which ones might work for you.

Disclaimer: This article contains affiliate links. If you open an account through these links, I may earn a commission at no additional cost to you. Investing involves risk, including the possible loss of capital. eToro is not available in all countries. Eligibility depends on your region. Always consider your individual circumstances before investing.

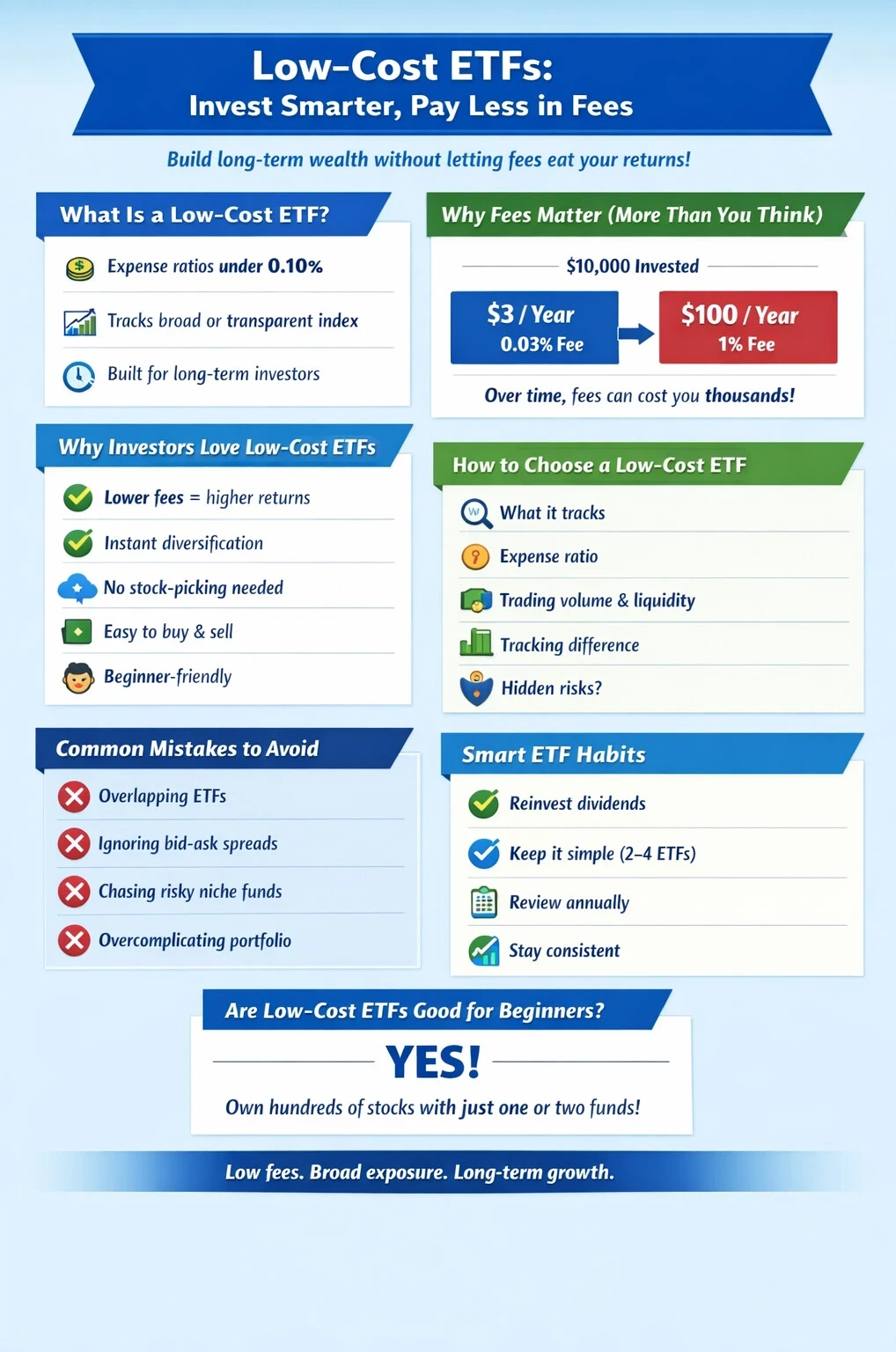

Why Low-Cost ETFs Are So Popular

Paying lower fees sounds great, but it’s more than just about saving a few bucks every year. Costs eat directly into your investment returns. Over several years, or even decades, these small numbers stack up and make a real difference. That’s one reason ETFs with low expense ratios attract a growing chunk of investors, both new and experienced. Plus, you get instant diversification without the need to pick and manage dozens of individual stocks on your own.

Some of the world’s largest asset managers, like Vanguard, BlackRock (iShares), and Schwab, have gone head-to-head to keep expense ratios at rock-bottom levels. This “fee war” has been a win for regular investors. If you’ve ever wondered exactly what you get for that fraction of a percent fee, or how these compare with more actively managed options, it’s worth checking out my post on the benefits of low-cost, high-yield ETFs.

How I Approach Picking Low-Cost ETFs

I usually look for a combination of a solid track record, a low expense ratio, and enough trading volume for smooth buying or selling. ETFs that closely track their index are also pretty important because you don’t want surprises in your performance versus the benchmark.

It’s easy to get lost in the small differences between almost identical funds, but there are a few questions I always ask myself before hitting “buy.”

- What is the ETF actually tracking? Sometimes, two funds with similar names are exposed to very different assets.

- How low are the fees? Even a 0.10% difference can add up over long holding periods.

- Is it traded widely enough? Funds with low trading volume can have bigger spreads. Those spreads quietly add to your costs.

- Are there any hidden risks? Some leveraged or niche ETFs look cheap but behave in unexpected ways.

If you want the full picture, there’s more about returns and averages in this guide to average returns for low-cost, high-yield ETFs.

Popular Low-Cost ETFs Worth Checking Out

I’ve worked with a few low-cost ETFs that get recommended again and again among investors. Here are some of the ones that show up the most in the low-fee crowd:

- Vanguard Total Stock Market ETF (VTI) – This one covers basically the entire U.S. stock market with an expense ratio of around 0.03%. If you want “set it and forget it” simplicity, this is a go-to choice for a lot of folks.

- Schwab U.S. Broad Market ETF (SCHB) – Similar style to VTI, with rock-bottom fees and great liquidity. It’s a solid alternative if you’re already set up with Schwab.

- SPDR S&P 500 ETF Trust (SPY) – SPY tracks the S&P 500, giving you exposure to the biggest U.S. companies. It’s got a slightly higher fee than some newer S&P competitors, but offers high liquidity and a long history.

- iShares Core S&P 500 ETF (IVV) – Also tracks the S&P 500 but usually sports a slightly lower expense ratio than SPY. It’s a smart pick if you’re counting every penny in fees.

- Vanguard FTSE Developed Markets ETF (VEA) – Tackles developed international markets outside the U.S., so you can mix in some global variety without paying up.

- iShares Core U.S. Aggregate Bond ETF (AGG) – For fixed income, AGG makes adding bond diversification simple and cheap.

Most of these funds trade on major stock exchanges, so you can pick them up straight from a broker or through platforms like eToro. If you want to look over prices, volume, or historical performance, TradingView is a super useful tool for checking charts and heat maps.

What to Know Before You Buy

Before splitting your paycheck into a handful of low-cost ETFs, I think it’s smart to consider a few practical things:

- Fees Still Matter: Low-cost doesn’t mean zero cost, so always double-check the stated expense ratio.

- Tax Considerations: Certain funds kick out capital gains distributions more than others, which can create surprise tax bills.

- Tracking Difference: Sometimes funds don’t match their benchmark exactly, especially during choppy or unusual markets.

- Underlying Holdings: Know what’s in the portfolio. Some “broad market” ETFs tilt heavily toward some sectors or big companies.

If you’re not sure where to spot a solid shortlist of affordable, high-yielding options, check my tips for tracking down low-cost, high-yield ETFs here.

Expense Ratios Explained

The expense ratio gets quoted as an annual percentage of assets, like 0.03% or 0.04%. Basically, that means for every $10,000 you keep in that ETF, you’ll pay $3 to $4 each year in fees. It’s a tiny bite compared to the 1% fees you might see with active mutual funds.

Liquidity and Bid-Ask Spreads

Even with low fees, ETFs with low trading activity can come with larger bid-ask spreads. That means you could pay a little extra on every trade if you’re not careful. I look for funds that move at least a few million dollars a day in trading volume as a simple rule.

Risks Specific to ETFs

Just because an ETF is cheap to own doesn’t mean it’s risk-free. If you’re picking a sector, country, or bond ETF, check how those underlying industries or economies are doing. Not all low-cost ETFs are as “safe” as the name might hint if they’re narrowly focused or highly leveraged.

Extra Tips for Using Low-Cost ETFs

I’ve picked up a few habits that make owning low-cost ETFs way smoother:

Reinvest Dividends – A lot of these funds pay out dividends. Reinvesting them automatically lets the returns compound, and you don’t even have to think about it.

Avoid Overlapping Funds – Having both VTI and SCHB, for example, means you’re doubling up on almost the same collection of stocks. I check the top holdings before stacking multiple ETFs.

Keep It Simple – I see a lot of beginners thinking they need a dozen ETFs to feel diversified. Often, two to four low-cost funds can cover the bases just fine. Your future self will thank you next time.

Stick to Your Plan – Markets will always have their ups and downs, but staying consistent with your investment approach is key. Don’t let short-term volatility tempt you to make sudden changes. It’s usually best to let your investments play out over the long haul.

Review Holdings Annually – Once a year, take a look over your ETFs and make sure they still fit your financial goals. If a fund changes its approach, or you notice creeping up in fees, be ready to switch to something simpler and more affordable.

Real World Applications from My Experience

When I first moved some of my money from active funds into low-cost ETFs, I noticed the drop in fees immediately. I paid less, and my portfolio performed just as well. Sometimes it did even better, thanks to fewer surprise trades and lower tax churn. I like to think of ETFs as the “sketchily” part of my portfolio, especially when paired with automatic monthly investments.

If you want to dig into the numbers or see how different ETF strategies compare, tools like TradingView let you look back with back testing, charts, and advanced tracking. Just pop in your ticker, and you’ll see historical data, price trends, and heat maps in a few clicks.

Frequently Asked Questions About Low-Cost ETFs

Can I buy these ETFs with zero commission?

Yeah, the good news is that many brokers, including some popular online platforms, offer zero-commission ETF trades these days. Check out eToro if you want a simple place to get started.

Are low-cost ETFs good for beginners?

They’re actually a favorite for those new to investing. With just one or two funds, you can own hundreds or even thousands of stocks. That takes a lot of guesswork out of picking individual companies.

Do low-cost ETFs pay dividends?

Most stock ETFs pay quarterly dividends that you can either take as cash or reinvest. Just read the fund’s details to see when and how much gets paid out.

Wrapping Up: Low-Cost ETFs in a Nutshell

Low-cost ETFs make it simpler and more affordable for people to build solid, long-term investment portfolios. Whether you’re saving for retirement or just getting started, these funds offer a practical way to keep more of your returns over the years. Remember to keep an eye on what you’re buying, know the fees, and avoid overcomplicating your lineup. With just a few of these in your portfolio, you’ll be ahead of the crowd, paying higher fees and missing out on compounding. Keep a cool head, revisit your holdings occasionally, and enjoy the benefits of long-term, low-cost investing.

Feel free to check out my other posts for more tips and hands-on guides to building your perfect ETF portfolio. There’s a lot more where this came from!