Understanding Low-Cost ETFs and Traditional Funds

Finding the right investment option can feel like trying to pick the right shoes for a hike. You want something that fits, works for your goals, and doesn’t break the bank. Two of the most popular ways people invest are through low-cost ETFs (exchange-traded funds) and traditional funds like mutual funds. Each has its strong points, but there are also a few tradeoffs. Knowing the difference helps you figure out what’s best for your situation, especially if you’re thinking long term or just trying to save on fees.

The last decade has seen a huge switch up toward low-cost investing, mostly because people want to keep more of their gains. Traditional mutual funds ruled the scene for a long time, but the rise of ETFs is mixing it up for how a lot of people think about building their portfolios. If you’re new to investing, it’s good to check out what makes these two approaches different and how that can impact your money down the line. For many investors, understanding these basics is the first step before jumping in with real money.

This article contains affiliate links. If you open an account through these links, I may earn a commission at no additional cost to you. Investing involves risk, including the possible loss of capital. eToro is not available in all countries. Eligibility depends on your region. Always consider your individual circumstances before investing.

What Are Low-Cost ETFs?

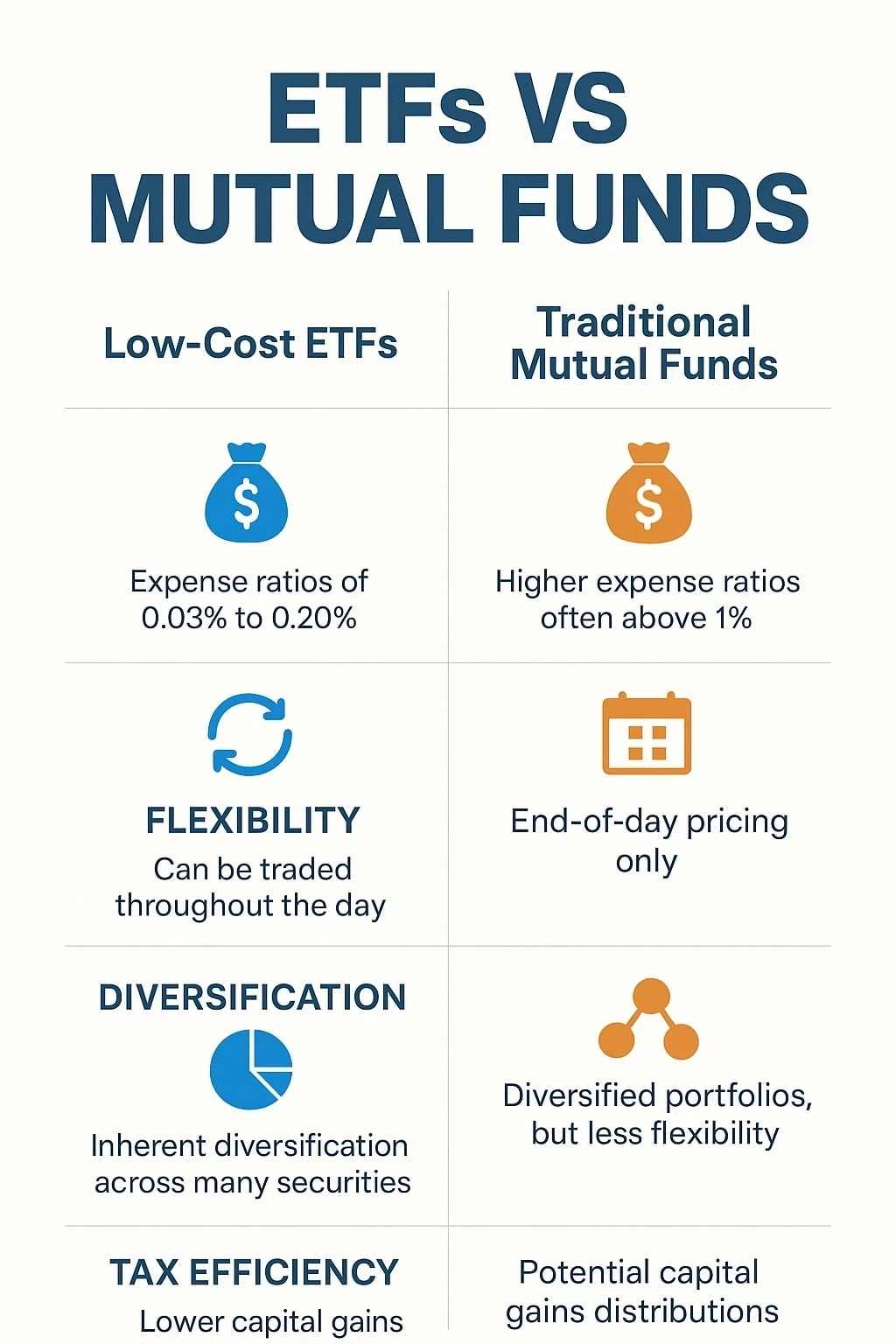

ETFs are basically investment baskets you can buy or sell on the stock exchange, kind of like stocks themselves. Low-cost ETFs are especially popular because they usually track major indexes (like the S&P 500) and don’t try to beat the market; they’re just trying to match it. The main thing that sets low-cost ETFs apart is, well, the price: their expense ratios are much lower than most traditional funds.

You’re able to buy and sell ETFs anytime the market is open, which is pretty handy for anyone who likes flexibility or wants to react quickly to market news. ETFs have grown so much in recent years that there are now options for almost every corner of the investment world: stocks, bonds, commodities, and even foreign markets. Some popular places to buy ETFs are through online brokers like eToro and TradingView.

- Expense Ratio: Most low-cost ETFs charge anywhere from 0.03% to 0.20% annually, which can save you a bunch over time.

- Tradability: Because they trade throughout the day like stocks, you can get in or out whenever you want (during market hours).

- Diversification: Even a single ETF can instantly spread out your risk across hundreds of securities.

What Are Traditional Funds?

Traditional funds, usually called mutual funds, have been around for decades. These funds bundle money from investors and put it into a selected pool of investments, which might be stocks, bonds, or a mix. You buy or sell shares of mutual funds at the end of the trading day based on the closing price (the net asset value or NAV), not during the day like ETFs.

There are a couple of types of traditional funds: actively managed funds that try to “beat the market” and passively managed ones that just aim to keep up with a benchmark. Actively managed funds tend to charge higher fees, since there are teams of analysts and managers picking stocks, and they sometimes rack up extra trading costs. These funds are popular for retirement accounts, workplace 401(k)s, or anyone who doesn’t want to think too much about timing the market.

- Expense Ratio: Actively managed mutual funds often have higher expense ratios, sometimes above 1% annually, which adds up.

- End-of-Day Pricing: You can only buy or sell at the end of the trading day, so there’s less flexibility for reacting quickly to market swings.

- Minimum Investments: Many mutual funds set minimums (sometimes $1,000 or more) to get started.

Comparing Fees and Costs

Keeping investment costs low is really important over the long run because fees can eat into your returns. Low-cost ETFs have taken off because their fees are often a small fraction of what you’d pay with actively managed mutual funds. Mutual funds sometimes also charge extra fees, like loads (sales commissions) or 12b-1 fees for marketing expenses, which can quietly chip away at your investments.

Here’s a quick breakdown of common costs:

- Expense Ratios: ETFs typically have expense ratios under 0.20%. Some mutual funds hit 1% or even higher.

- Front or Back Loads: Mutual funds can charge you when you buy (front load) or sell (back load) the fund. Low-cost ETFs usually skip these charges.

- Trading Fees: ETFs may have a trading fee or commission, but many platforms, like eToro and TradingView, offer commission-free trades on popular ETFs.

Liquidity and Flexibility

One thing I like about ETFs is how flexible they are; you can buy and sell throughout the day and even use advanced orders like stop-loss or limit orders. This flexibility is a big deal for anyone who cares about market timing or just wants faster access to their money.

Mutual funds don’t offer that same freedom. All transactions are settled at the end of the day, which can be a downside if the market is moving a lot or you need to make quick changes. For some investors, especially those with a “set and forget” approach, this isn’t a dealbreaker, but it’s good to know if you value flexibility in your investments.

Tax Efficiency

Taxes can make a real difference to your returns, and ETFs usually have a tax advantage. Because of how they’re structured, ETFs rarely pass on capital gains taxes to investors unless you actually sell your shares. Mutual funds, on the other hand, sometimes distribute taxable capital gains to everyone who owns the fund, often at the end of the year, even if you haven’t sold a thing.

This means you can sometimes get hit with an unexpected tax bill just for holding onto a mutual fund. This tax efficiency edge is one reason ETFs are a popular pick for taxable investment accounts.

Minimum Investments and Accessibility

Low-cost ETFs are open to just about any budget. You can buy as little as a single ETF share (or even fractions of a share with some brokers), making them great for anyone who wants to start small. Mutual funds sometimes require a bigger upfront investment, so beginners on a tight budget might find it harder to get started there.

With user-friendly platforms like eToro and TradingView, getting started with ETFs is pretty straightforward. These platforms often have low account minimums and smooth the way to track your investments in real time. In addition, educational resources and built-in tools make these platforms attractive for new and experienced investors alike.

Management Style: Active vs Passive

Most ETFs are passively managed, tracking an index or sector rather than picking stocks. This keeps fees low and removes a lot of the guesswork. Mutual funds come in both types: active and passive. Actively managed funds sometimes outperform, especially in strange or inefficient markets, but they also come with higher expenses and the risk of underperforming after fees. If you like the idea of hands-off investing, low-cost ETFs might be the way to go. But there are some investors who like having a pro calling the shots, hoping that extra research gives them an edge.

Potential Drawbacks to Watch Out For

No investment approach is perfect. Here are a few things to consider before jumping into low-cost ETFs or traditional funds:

- Trading Costs: While most ETF trades are free on major platforms now, smaller or less liquid ETFs could have wider bid-ask spreads, which bump up your cost to buy or sell.

- Overtrading: Because ETFs trade like stocks, it’s easy to get carried away. Sometimes, frequent trading can hurt your long-term performance if you aren’t disciplined with your strategy.

- Tracking Error: Sometimes, an ETF doesn’t track its benchmark exactly, usually by a tiny margin. Most of the time, this isn’t a big deal, but it’s worth checking if accuracy is important to you.

- Minimums and Fees: With mutual funds, look out for minimum investment requirements and extra fees that can pop up, especially with actively managed funds.

Liquidity

Most popular ETFs are super liquid, but niche or specialty ETFs might not have many buyers and sellers. It’s good practice to check trading volumes before investing in something off the beaten path. Mutual funds don’t have this issue since the fund company is buying or selling at the NAV, but again, you lose some flexibility there.

Transparency

ETFs are required to disclose their holdings every day, which is pretty handy if you want to see exactly what you’re buying. Mutual funds report their holdings quarterly, so you get less frequent updates and might be in the dark about recent changes to what you own. Thorough transparency can help investors stay informed and make smarter choices as markets change.

RealWorld Examples and Use Cases

Picture someone just getting started with investing with a few hundred bucks. An S&P 500 ETF offers instant diversification, low fees, and flexibility. That same person might find it tough to meet the $1,000 minimums for many mutual funds, especially if they’re just testing the waters or want to build a portfolio gradually.

Someone saving for retirement and investing through a workplace plan might have easier access to mutual funds, with automatic contributions and built-in rebalancing. Some mutual funds also have automatic dividend reinvestment and low transaction costs, which can be a plus for retirement savers. Either way, matching your investment style to your needs usually pays off more than just picking based on fees alone.

- ETFs for DIY Investors: If you want control, real-time trading, and ultralow fees, ETFs are tough to beat.

- Mutual Funds for Handsoff Investors: Automatic reinvestment, professional management, and set-and-forget simplicity make mutual funds a popular choice for retirement plans.

Frequently Asked Questions

Which is better for beginners: Low-cost ETFs or traditional funds?

Both have their upsides, but low-cost ETFs are super accessible for smaller budgets and anyone who likes flexibility. Traditional funds might make sense if you prefer hands-off investing or have access to solid, no-load mutual fund options in your retirement plan.

Do ETFs pay dividends?

Yes, many popular ETFs pay dividends. Some automatically reinvest them (called “accumulating” ETFs), while others pay them out in cash (“distributing” ETFs).

What’s the main risk of low-cost ETFs?

Market risk is the main one. They’ll go up and down with the index they track. Also, overtrading because of how easy it is to buy and sell can actually hurt long-term performance if you’re not careful.

Final Thoughts

Both low-cost ETFs and traditional funds can help you reach your financial goals, and each has some clear pros and cons. For most people, starting with a low-fee ETF portfolio is a solid way to begin investing, especially if you want to keep things simple, affordable, and flexible. If you’re working with a bigger budget or want extra guidance, checking out a few high-quality mutual funds might not be a bad idea.

A mix of both works for a lot of investors; just make sure you look closely at costs, check the trading features, and stick to your plan as your money grows. Whatever you choose, making informed decisions is really important in keeping your financial adventure on track. Platforms like eToro or TradingView are worth checking out if you want to track down these options for yourself.