If you’re aiming for a comfortable retirement, picking low-cost ETFs (exchange-traded funds) can be pretty handy for stretching your savings further. High investment fees can quietly chip away at your returns, so keeping costs low helps your money grow. In this article, I’ll break down what makes a low-cost ETF ideal for retirement accounts and help you sort through options without feeling overwhelmed.

Understanding Low-Cost ETFs for Retirement

Low-cost ETFs are funds that track a specific index, sector, or asset class, but with much lower fees compared to active mutual funds or standard ETFs. Over decades, even a half-percent difference in fees adds up to thousands of dollars. That’s why low-cost ETFs are really popular with long-term investors, especially for retirement accounts like IRAs or 401(k)s.

Many major brokerages and fund families, like Vanguard, Schwab, and iShares, now offer index ETFs with annual expenses as low as 0.03% to 0.10%. If you’re investing for the next 20, 30, or 40 years, those fee savings can make a big difference in how much you’ll actually have at retirement.

Besides low fees, these ETFs give you instant diversification—you can own hundreds or even thousands of stocks or bonds in just one single fund purchase. That makes portfolio building and rebalancing much easier, and the transparency is a nice bonus since you can see exactly what you own at any point. Plus, you can use fractional investing with many brokers, making it easy to start with even small amounts of money.

Key Benefits of Low-Cost ETFs for Retirement

I like low-cost ETFs for retirement because saving on fees is just one of their advantages. Here’s what really stands out for long-term investors:

- Lower Cost: The expense ratio is the percentage of your investment that goes to fees each year. Keeping this number below 0.20% means more of your returns get reinvested for growth. Even a 1% fee difference over 30 years on $50,000 could mean the difference between retiring with $174,000 or $146,000 (assuming a 6% annual return, just as a rough comparison).

- Diversification: With just one or two ETFs, you can cover the entire US stock market, international companies, or a mix of bonds. That instant spread helps smooth out the bumps if one area takes a hit.

- Tax Efficiency: ETFs have a special structure that often results in fewer capital gains distributions, so your taxable accounts can potentially keep more of those gains growing tax-deferred, which adds up over time.

- Easy to Buy and Sell: ETFs can be purchased or sold any time the market is open, and most major brokerages let you trade them commission-free.

All these perks add up to a smoother retirement investing experience for most people. If you’re already using a robo-advisor, you’re probably invested in low-cost ETFs, whether you realize it or not. But if you’re handling things on your own, a handful of ETFs is usually all you need.

Top Types of Low-Cost ETFs for Retirement Portfolios

The range of ETFs can get kind of wild, but for retirement savings, I stick to core options that cover big sections of the market. These are some of the most common types:

- Total US Stock Market ETFs: Tracks the entire US stock market, from Apple down to tiny companies you’ve never heard of. Examples: Vanguard Total Stock Market ETF (VTI), Schwab US Broad Market ETF (SCHB).

- US Large Cap ETFs: Focuses on big, established companies like Microsoft, Johnson & Johnson, and Google. Examples: SPDR S&P 500 ETF Trust (SPY), iShares Core S&P 500 ETF (IVV).

- Total International Stock Market ETFs: Gives you exposure to companies outside of the US. Examples: Vanguard Total International Stock ETF (VXUS), iShares Core MSCI Total International Stock ETF (IXUS).

- Bond ETFs: Great for lowering risk, these track government, corporate, or international bonds. Examples: Vanguard Total Bond Market ETF (BND), iShares Core US Aggregate Bond ETF (AGG).

- Target Date or Asset Allocation ETFs: Automatically adjust your mix of stocks and bonds as you get closer to retirement. Examples: iShares Core Growth Allocation ETF (AOR), Vanguard Target Retirement ETFs.

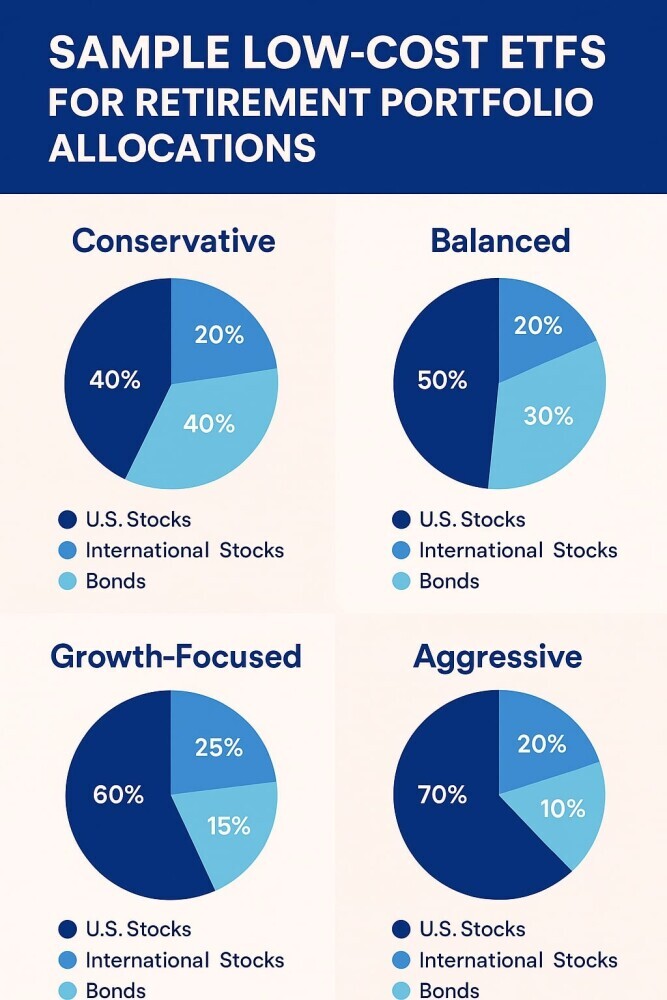

Mixing a few of these ETFs gives you a balanced portfolio that doesn’t require a ton of attention. For example, lots of investors will go 60% stocks (using VTI) and 40% bonds (using BND), or split things more globally using VXUS or IXUS. You can always dial up or down the risk based on your comfort zone and age.

Some people also like to add a small segment of sector or dividend ETFs for extra flavor, such as real estate or utilities funds. However, the bulk of your retirement money should go into broad, low-cost options to keep things simple and reduce the chances of making costly mistakes.

How to Choose the Right Low-Cost ETFs for Your Retirement

Picking the “best” ETF can feel stressful, but it’s really about finding solid quality at a good price. Here are the main things I look for:

- Expense Ratio: I like to see these below 0.10%, and definitely under 0.20% for broad market ETFs.

- Volume and Liquidity: Bigger funds are generally easier to buy and sell without extra cost. Look for big names with lots of trading each day.

- Tracking Error: This tells you how closely the ETF follows its index. Lower is better, since you want performance to match what you signed up for.

- Holdings Transparency: Does the fund clearly list which stocks or bonds it owns? Most reputable ETFs have daily updates.

- Issuer Reputation: Vanguard, Schwab, BlackRock/iShares, and Fidelity are the major players with long track records of serving retirement investors.

Just as important: know what you’re investing in. If an ETF promises market-beating returns with a strange strategy and a high fee, that’s definitely a reason to slow down and do more research. You want steady, predictable funds for retirement savings, not the latest eye-catching trend.

Potential Downsides and What to Watch For

Even the cheapest ETF isn’t always a match for every investor. Here are a few things that can trip people up:

- Market Risk: Low-cost ETFs still go up and down with the market. If you panic and sell at the wrong time, you could lock in losses.

- Over Diversification: Some people stack up too many ETFs and end up buying the same companies in different funds. Stick to one or two that broadly represent stocks or bonds, unless you’ve got a plan for niche investing.

- Chasing Trends: New ETFs pop up all the time, promising great new strategies. If the expense ratio is higher or the idea is complex, it’s usually worth skipping for core, tried-and-true funds.

- International Tax Issues: If you’re investing in international ETFs inside a taxable account, you might run into some extra paperwork or taxes on dividends. In retirement accounts, this usually isn’t a big deal, but it’s something to ask your tax advisor about.

Smart investing means doing your homework, not just chasing what’s new or trendy. Reliable low-cost ETFs have strong track records because they stick to simple strategies that work for the long haul. It pays to keep an eye out for changes in expense ratios, and it’s smart to review your investments now and then.

Common Questions About Low-Cost ETFs and Retirement

People ask a lot of questions before putting money into ETFs for retirement. Here are a few I get a lot:

Q: Can you use low-cost ETFs in both IRAs and taxable accounts?

Low-cost ETFs work in any account, and a lot of people use them in both. Taxable accounts get some benefit from the tax efficiency, but retirement accounts make the most of long-term compounding without worrying about yearly taxes.

Q: Do I need to rebalance my ETF portfolio?

Yes, checking your balance once or twice a year is really important. If your stocks jump way up, your account could become riskier than you want, so selling a little and buying more bonds (or vice versa) helps keep things on track.

Q: Are low-cost ETFs always safer than other investments?

Safety depends on what the ETF holds. A low-cost stock ETF still moves with the market. The lower fee helps your long-term growth, but it doesn’t make the fund less volatile. Mixing in bond ETFs can lower risk overall.

Q: Can I start with just a small amount in ETFs?

Absolutely. Many brokers now let you buy ETF shares in small increments thanks to fractional shares. This makes it easy for new investors to start building a portfolio with even modest amounts, and lets you steadily add more over time.

Practical Steps for Building Your Low-Cost ETF Retirement Portfolio

I like to keep things really simple. Here’s a sample setup you can tweak to your own needs:

- Pick one total US stock ETF (like VTI or SCHB).

- Add an international ETF (like VXUS or IXUS) for more global exposure.

- Add a bond ETF (like BND or AGG) to smooth out the ride.

- Set an allocation you can stick with (a popular split is 60% US stocks, 20% international, 20% bonds).

- Rebalance each year or when your allocation drifts a lot.

Automatic investing plans at brokers make this even smoother. Just set your deposit and let it ride. If target-date ETFs appeal to you, those are even more hands-off; they do the allocation and rebalancing for you as you age. If you want help, many brokers have online tools and calculators to help you determine your risk tolerance or optimal allocation, so you don’t have to guess at every step.

Wrapping Up

Low-cost ETFs have changed how people invest for retirement, giving anyone access to broad markets, steady returns, and low fees without needing to be a finance expert. By focusing on core funds, watching your costs, and rebalancing now and then, it’s easier to build a portfolio that keeps working for you as you head toward retirement. If you’re just getting started, stick to simple, low-fee funds from trusted providers, and reach out to a financial advisor if you want a second opinion. You don’t have to pay big fees to make your money work harder; just a little research and some steady habits go a long way.