Low-cost high yield ETFs are popping up everywhere, promising steady income and affordable access to markets. Plenty of people are eyeing them for their retirement portfolios with the hope of growing their nest egg without paying steep management fees. I’ve dug deep into how these ETFs actually work for long-term savings, what to watch out for, and some practical tips to make the most of them if you’re thinking about your retirement goals.

Disclaimer: This article contains affiliate links. If you open an account through these links, I may earn a commission at no additional cost to you. Investing involves risk, including the possible loss of capital. eToro is not available in all countries. Eligibility depends on your region. Always consider your individual circumstances before investing.

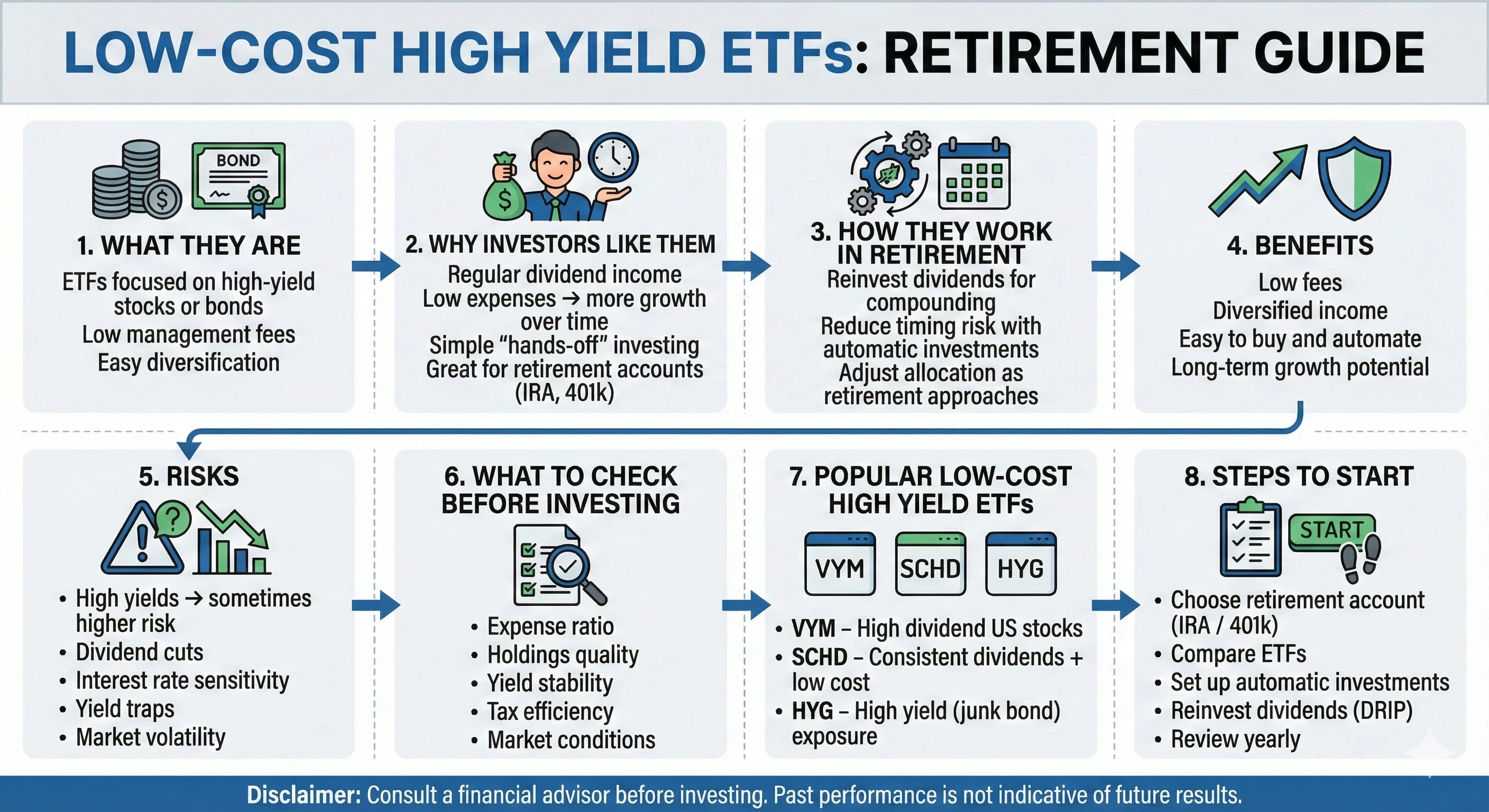

Understanding Low Cost High Yield ETFs

Exchange traded funds (ETFs) have made it easy for everyday savers like me to build a diverse set of investments without spending a lot on management fees. A high yield ETF usually targets baskets of dividend paying stocks, bonds, or other assets that aim to give out above average income. When these are also low cost, you get the power of hands off diversification and potentially higher yields for less out of your pocket. This approach suits busy investors or those just starting out, since it saves both time and money compared to picking individual stocks.

Some of the most popular examples are ETFs that track high yield corporate bonds, dividend focused stock ETFs, or even international high dividend strategies. Over the last decade, the growth of these ETFs shows just how much people want simple, income producing investments, without the sticker shock of traditional funds. If you’re keen to see how these ETFs have performed or want concrete data, TradingView can be super helpful for checking historical returns and comparing funds side by side.

How These ETFs Work for Retirement Savings

When you buy a low cost high yield ETF, you’re essentially pooling your money with a bunch of other investors to buy dozens or even hundreds of high yielding assets. If one stock or bond has a rough year, the impact on your whole retirement account can be cushioned since you’re spread out across the fund’s entire portfolio. The low expense ratio means more of your investment goes into growing your account rather than feeding hefty management fees year after year.

The real appeal for retirement savers is in the compounding power of reinvesting those high yields over decades. If you funnel dividend payouts back into more ETF shares, you can speed up your account’s growth. Even if retirement feels a long way off, that regular cash flow can eventually help cover living expenses once you stop working.

Besides regular dividends and long term growth, using ETFs in retirement plans also gives you flexibility. You can sell shares if you need cash, or adjust your allocations based on changes in your goals as you near retirement. This versatility means you stay in control without getting bogged down by complex investment choices.

Steps to Add Low Cost High Yield ETFs to Retirement Accounts

- Pick Your Retirement Account: Most people use IRAs or 401(k)s for long term savings because of their tax advantages. Both traditional and Roth versions let you invest in ETFs through many online brokers.

- Research Fund Choices: Compare expense ratios, yield history, and what’s actually inside the ETF. Try platforms like eToro to find top ETFs and read user reviews.

- Set Up Automatic Investments: Most brokers will let you schedule recurring buys. Automating your contributions means you’re dollar cost averaging over time, which helps reduce the risk of bad timing.

- Reinvest Dividends: Check that your broker offers a dividend reinvestment option (“DRIP”), which puts those payouts right back to work inside your ETF.

- Review and Adjust: Once or twice a year, take a look at your holdings and see if anything is drifting away from your risk tolerance or goals.

Going step by step like this helps you establish good habits and stick with your plan even during volatile market periods. Consistency is your friend, especially when you have many years before retirement.

Potential Benefits and Drawbacks

Any investment has its trade offs. Low cost high yield ETFs shine for quite a few reasons, but there are also downsides that I always keep in mind.

- Benefits: Super simple diversification, low ongoing fees, regular income, and easy hands off growth. The combination is pretty attractive if you’re after a straightforward plan and don’t want to manage individual stocks or bonds.

- Drawbacks: High yields can sometimes point to risky underlying assets, like junk bonds or troubled companies. There’s no guarantee those high payouts will keep rolling in during market downturns. Yields can also fluctuate over the years, and certain ETF structures might pile on tax headaches if you buy them outside retirement accounts.

Also, the market value of high yield ETFs can drop when rates rise, or during economic stress. This makes it important to balance income expectations with a realistic view of the risks involved.

Key Considerations Before Investing

Here are points that help me decide if a low cost high yield ETF actually fits into my retirement strategy:

- Expense Ratio: Lower is almost always better. Over decades, just half a percent in costs can chew away a big chunk of growth.

- Underlying Holdings: Check what the ETF owns since junk bonds, emerging market stocks, or ultra high yield businesses might bring more income but add more risk too. I recommend using TradingView to visualize holdings and sector exposure.

- Yield Consistency: It’s smart to look for funds with a long record of maintaining, or even growing, their payouts, not just the highest yield out there today.

- Tax Efficiency: Some high yield ETFs kick off a lot of taxable income, which isn’t a concern inside IRAs or 401(k)s but could hurt in a regular brokerage account.

- Market and Interest Rate Cycles: Yields and share prices can move with the broader market or changes in interest rates. Stay flexible and don’t expect the same returns every year.

Remember to review your risk comfort level and adjust your holdings if big life changes happen, such as a new job or approaching retirement. Looking at your overall financial picture will help you feel confident about your ETF choices.

Common Challenges with High Yield ETFs

- Yield Traps: Sometimes, those massive yields are because the underlying stocks or bonds are in trouble. It pays to dig deeper if something looks too good to be true.

- Interest Rate Changes: Bond focused high yield ETFs can take a hit if interest rates rise quickly, which can push prices down. It’s less of a problem if you’re buying regularly over a long period, but it’s worth being aware.

- Dividend Cuts: Companies can always lower or even scrap their dividends during tough times. If you’re relying on ETF payouts to cover expenses, that can sting.

- Liquidity: Some niche high yield ETFs might be thinly traded, making it harder to buy or sell at good prices.

Keep an eye on the news and quarterly ETF updates so you’re aware of any big changes that could affect your holdings. Staying on top of these common issues lets you act quickly and protect your long-term savings.

Expense Ratio Spotlight

The expense ratio is just the annual fee to keep the ETF running. If one fund charges 0.08% and another has 0.70%, that gap can really add up over 20 to 30 years. You can usually find this info on the ETF’s main page on your broker’s website or through resources like eToro. Make sure to compare several options before settling on one, since a lower expense means more money stays in your pocket.

Consistency and Volatility

Chasing the highest yield each year isn’t always the smoothest ride. I’ve seen dividend focused ETFs swing a lot in both yield and market price, so I try to balance these out with other growth or balanced funds in my retirement plan. That way, one bad year won’t throw everything off. Mixing consistent low cost index funds with high yield ETFs can help you manage volatility and keep returns steadier over time.

Real World Examples of Popular Low Cost High Yield ETFs

- Vanguard High Dividend Yield ETF (VYM): Focuses on large U.S. companies with high dividend yields. The expense ratio is usually under 0.10% and the holdings are widely diversified.

- iShares iBoxx $ High Yield Corporate Bond ETF (HYG): Tracks high yield corporate (junk) bonds with a steady payout, though sometimes with higher price swings.

- Schwab U.S. Dividend Equity ETF (SCHD): Popular for its mix of high yield and consistency, along with a low cost structure.

These are just a few options worth checking out. Researching yield history and sector mix on comparison sites will help you spot which ones feel right for your needs. You can find many high yield ETFs that focus on different sectors, regions, or types of assets, so it pays to match your choice to your financial goals and time horizon.

FAQ: Using High Yield ETFs for Retirement

Can I use only high yield ETFs for my retirement portfolio?

Using only high yield ETFs might leave you too exposed to specific risks or market shifts. Mixing in some growth or balanced ETFs can give smoother results over the long run.

Is it safe to put all my retirement money in these funds?

No investment is 100% safe. Spreading your money across different asset types and ETFs helps reduce risk compared to betting it all on one kind of fund or market sector.

Do I pay tax on ETF dividends in my retirement account?

Inside an IRA or 401(k), taxes on dividends and growth are deferred (or tax free with Roth accounts), but in a standard brokerage account, you’ll owe taxes on annual payouts.

Can I buy these ETFs easily?

Most large low cost high yield ETFs are traded daily on major exchanges, so they’re easy to buy or sell with just a few clicks through most brokers.

Wrapping Up: Building Your Retirement with Low Cost High Yield ETFs

Low cost high yield ETFs can be a practical way to crank up your retirement savings thanks to their income focus and affordability. Checking out fund details, understanding your risk tolerance, and automating your approach can help build more confidence no matter what the markets do. For more data, side by side comparisons, or to take the next step, platforms like TradingView and eToro make it easier than ever to research and invest.

Focusing on long term consistency over chasing quick wins keeps stress levels low and your savings growing toward the retirement you’re dreaming about. Making use of these strategies and resources will help you build a solid foundation for a comfortable future, no matter how the market changes.